Travel money and foreign exchange news, views and articles on the Compare Holiday Money blog

The dirham is the official currency of the United Arab Emirates. Find out how to get the best dirham rate by comparing suppliers on Compare Holiday Money.

2 comments

2 comments

Enjoy a few extra euros in your holiday wallet this summer as the pound strengthens against the euro.

1 comments

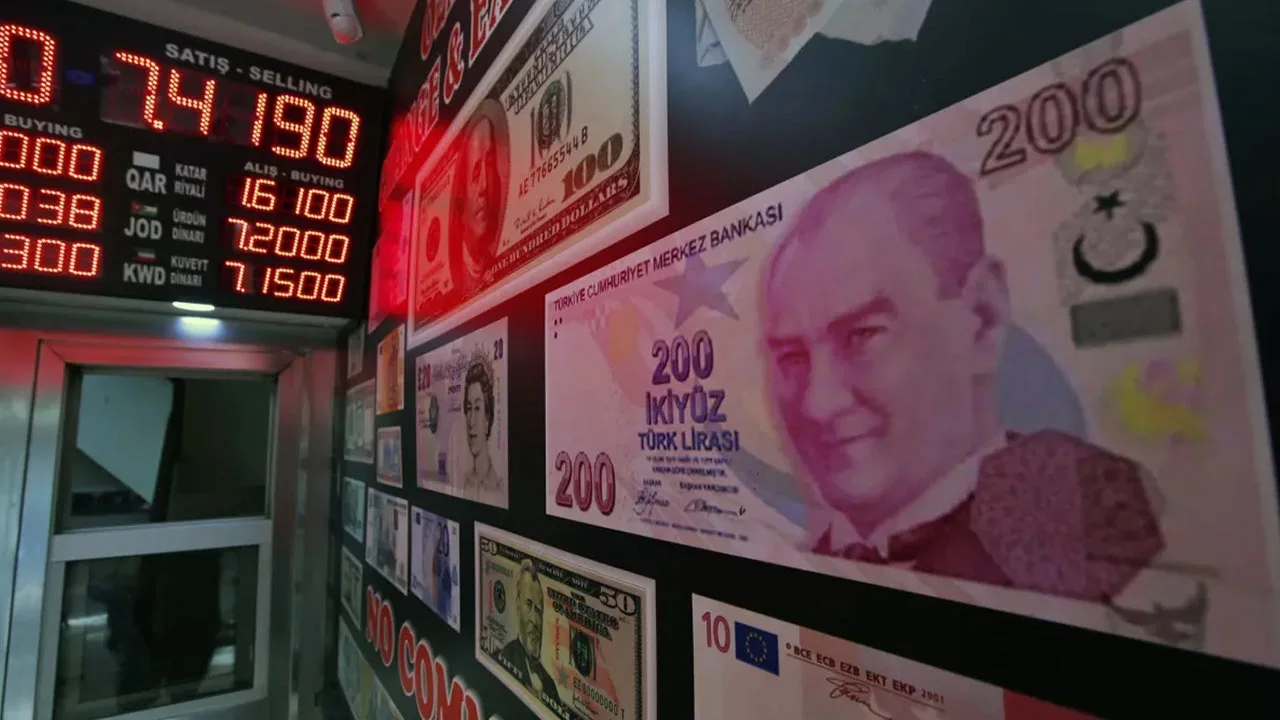

The plunging Turkish Lira rate can offer excellent value for money for British holidaymakers - if you're prepared to get off the beaten track.

1 comments

Have a memorable holiday for all of the right reasons this summer with our tips for staying safe abroad.

2 comments

The lira's dramatic decline continues as Turkey's re-elected President Erdogan appoints a new economic team to address the country's precarious financial state.

5 comments

Croatia has officially withdrawn the Croatian kuna and replaced it with the euro.

Football fans are advised to plan ahead and follow the Foreign and Commonwealth Office's travel advice for the Qatar 2022 World Cup.

GHIC is a free card issued by the NHS that entitles you to emergency state-provided healthcare when you’re visiting an EU country or Switzerland.

The Swiss franc is the official currency of Switzerland, Liechtenstein, and the tiny Italian exclave of Campione d'Italia.

2 comments

Mexico is a relatively good value holiday destination for British travellers. Find out how many pesos you should budget for your trip.

3 comments

A strong pound means higher exchange rates and a better deal for UK travellers.

2 comments

We take a look at some of the most expensive countries to visit in Europe.